- Everyday Alpha

- Posts

- This Gas Turbine Name Is Forcing a Second Look from Energy Bulls

This Gas Turbine Name Is Forcing a Second Look from Energy Bulls

A major turbine win just lit the fuse for this stock, yet its valuation still trails earnings potential as global LNG and power demand accelerate.

Noah Zelvis

February 13, 2026

Energy security is driving real infrastructure spend, not just headlines. This gas-focused powerhouse has demonstrated that demand is alive and the market may still be underestimating what comes next. Are you?

Big Upside (Sponsored)

A new research report highlights 5 stocks with the strongest potential to double in the year ahead.

Each was selected from thousands of companies and shows a rare mix of:

Strong fundamentals

Bullish technical setups

Past versions of this report delivered gains of +175%, +498%, and even +673%¹ — and the latest edition is free for a short time.

Available only until MIDNIGHT TONIGHT.

Download the free report

Never Miss a Stock Alert Again!

We now send our daily picks via text too — so you’ll get the same high-conviction ideas, even if you miss the email.

Baker Hughes Company

February 13 – Pre‑market

Ticker: BKR | Sector: Oil & Gas Equipment & Services / Energy | Market Cap: ~$60.6B

30‑Second Take

Something just shifted. Baker Hughes landed a major gas turbine contract, and the market did not shrug.

This is a company leveraged to global LNG buildout, power demand, and gas infrastructure investment at a time when energy security is no longer optional.

And even after a 28% gain, it is still undervalued by around 23%.

Fresh contract momentum. Explosive price action. A valuation gap that has not closed. This kind of window doesn’t usually stay open for long.

Trade Setup

Time frame: Medium term

Edge type: Fundamental re-rating with contract-driven momentum

This is not a quick scalp after a headline spike. The recent move signals institutional accumulation tied to real order flow, not retail euphoria.

The edge lies in earnings visibility, which is improving faster than sentiment. If turbine demand and LNG infrastructure spend continue to stack up, the multiple can expand alongside estimates.

Rare Access (Sponsored)

For decades, one type of investment was reserved for the ultra-wealthy.

Then Trump signed Executive Order 14330 - and opened it to everyone.

Now you can get into this boom for less than $20.

See what changed

Trivia: In 1979, which company introduced the first portable cassette player that reshaped music consumption and monetization? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $61.39 | Average |

52‑week range | $33.60 - 62.27 | Average |

Short interest | 2.71% | Below average |

Next catalyst | Backlog expansion update |

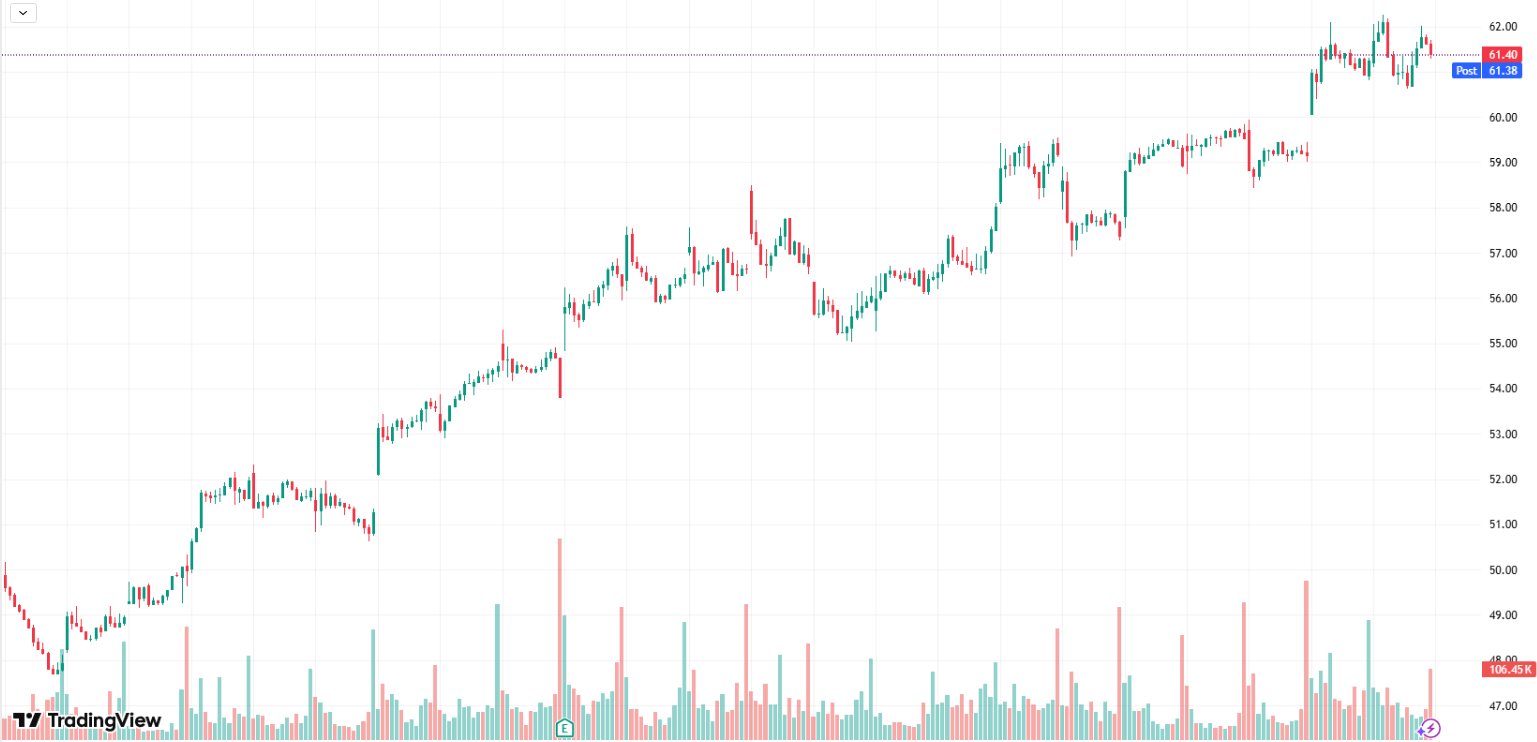

Chart

1-month trading summary: BKR is up 27.28% in the past month and pressing right into its 52-week highs near $62.00.

The move has been stair-stepped, not parabolic. Higher highs, higher lows, and constructive pullbacks along the way. That is accumulation, not exhaustion.

Volume has not exploded, which actually strengthens the case. This looks like steady institutional buying rather than a blow-off top.

Technically, it is coiling just beneath a breakout level. If it clears and holds above the $62.00 area, the next leg higher could come quickly.

Bull Case

The market is still underestimating this gas infrastructure engine: Baker Hughes is no longer an oilfield services name riding commodity cycles.

It’s a leveraged play on global gas infrastructure, LNG expansion, and power generation demand, which are structurally reshaping energy markets.

The recent gas turbine contract is not a one-off win. It is proof that utilities, LNG developers, and industrial players are still spending aggressively to secure reliable power.

Gas is the bridge fuel of choice, and Baker Hughes sells the hardware that makes that bridge possible. It’s right at this point in the story that things get really interesting.

As global LNG capacity expands and emerging markets demand more stable electricity, turbine orders and services revenue compound.

That mix shift toward higher-margin, longer-cycle infrastructure contracts improves visibility and earnings quality. It is not just revenue growth. It is better revenue.

Despite the near 28.00% surge, the stock is still meaningfully undervalued relative to its forward earnings power.

If order momentum continues and margins hold, we are not talking about a trade driven by oil price noise. We are talking about a multi-quarter re-rating tied to durable capital investment.

Order flow that forces attention: The turbine contract was the spark. What matters now is the force and durability of that fire.

The first catalyst is additional large-scale gas turbine or LNG equipment awards. A second or third headline win would signal that this is a trend, not a one-off.

Next is backlog expansion. If upcoming updates show a step-change in backlog tied to gas infrastructure and power, the earnings visibility argument strengthens immediately.

Then come margins. If management demonstrates operating leverage from a higher-margin turbine and services mix, estimate revisions follow.

Price targets lag the tape: Analysts are also undervaluing BKR, with the high price target sitting at $68.00, not too far off current stock prices. The low is $44.00.

Breakout pressure building: BKR is pressing right up against its 52-week highs with higher highs and shallow pullbacks, suggesting accumulation rather than exhaustion.

A decisive push through resistance could trigger momentum buyers and force short-term repositioning higher.

Bear Case

Execution must match the narrative to support the bull case: The biggest risk here is simple. The story could be running ahead of the numbers.

Gas turbines grab headlines, but these are complex, capital-intensive projects with long delivery cycles. Cost overruns, supply chain friction, or margin compression could quickly dent the re-rating case.

There is also cyclicality lurking beneath the infrastructure glow. If global LNG final investment decisions slow or energy capex tightens, order momentum can fade just as quickly as it appeared.

Fighting for the next megaproject: This here is the heavyweight division.

On the turbine and power side, GE Vernova and Siemens Energy are entrenched with utilities and national energy champions. They have scale, balance sheet muscle, and long-standing service contracts that create sticky relationships.

On the oilfield services front, SLB and Halliburton continue to push on technology differentiation and capital discipline, often winning investor favor when margins expand cleanly.

The competitive risk here is subtle but real. If the next wave of LNG and power awards tilts toward those names, or if they show cleaner execution and margin lift, the re-rating case for Baker Hughes loses some of its edge.

In this space, perception shifts quickly, and capital follows performance.

LNG timing and capex discipline: Baker Hughes is tied directly to large-scale LNG and gas infrastructure investment.

If final investment decisions on new LNG terminals are delayed due to regulatory friction, financing constraints, or political pushback, turbine and equipment orders can slip.

There is also capital discipline across energy producers. If oil and gas majors tighten spending or prioritize shareholder returns over expansion, demand for upstream and midstream equipment softens.

For Baker Hughes, this is not about daily oil price swings. It is about whether the global gas infrastructure buildout stays on schedule.

Momentum money piling in: After a near 28% one-month surge into 52-week highs, short-term momentum capital is clearly involved.

If positioning gets crowded and the next update is merely good rather than great, fast money could unwind quickly, amplifying downside volatility.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (February 12, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha