- Everyday Alpha

- Posts

- This Beaten-Down Biotech Has Reinvented Itself as a Revenue Machine

This Beaten-Down Biotech Has Reinvented Itself as a Revenue Machine

Explosive revenue growth and extreme short interest are colliding in this small-cap oncology name. The science is now commercial, and the pressure to position is building.

Noah Zelvis

February 25, 2026

For years, this was a dilution-heavy biotech that traders loved to fade.

Now, revenue is scaling, momentum is building, and a massive short base is betting it will fail. Where are you positioned?

Prior Winners (Sponsored)

From thousands of stocks, only five stood out as having the best chance to gain +100% or more in the months ahead.

A newly released 5 Stocks Set to Double special report reveals all five tickers — free for a limited time.

While future results can’t be guaranteed, previous editions of this report delivered gains of +175%, +498%, and even +673%¹.

The newest picks could follow a similar path.

This free opportunity expires at MIDNIGHT TONIGHT.

Get the free report here

*This free resource is being sent by Zacks. We identify investment resources you may choose to use in making your own decisions. Use of this resource is subject to the Zacks Terms of Service.

*Past performance is no guarantee of future results. Investing involves risk. This material does not constitute investment, legal, accounting, or tax advice. Zacks Investment Research is not a licensed dealer, broker, or investment adviser.

Never Miss a Stock Alert Again!

We now send our daily picks via text too — so you’ll get the same high-conviction ideas, even if you miss the email.

ImmunityBio, Inc.

February 25 – Pre‑market

Ticker: IBRX | Sector: Biotechnology / Healthcare | Market Cap: ~$11.3B

30‑Second Take

ImmunityBio, Inc. just reported roughly 700% year-over-year revenue growth. That is not biotech hype. That is commercial ignition.

For years, this was a capital-intensive development story weighed down by dilution, delays, and skepticism.

Now it has an approved product, accelerating unit sales, and triple-digit quarterly revenue growth. The narrative has shifted from survival to scale.

Trade Setup

Time frame: Short to medium term

Edge type: Commercial inflection + sentiment reset + momentum continuation

For years, IBRX was treated like a perpetual capital raise with a science project attached. That perception lingers.

Meanwhile, revenue is scaling aggressively, and the company is operating like a commercial-stage oncology business.

The edge sits in that gap.

One Voice (Sponsored)

$1,000 in just seven stocks in 2004 could have turned into a million-dollar portfolio today…

Back then… one financial expert begged people to look at Nvidia -- when it was trading at just $1.10!

Now… he’s urging you to look at a new group of seven stocks…

Check this Out (The NEXT Magnificent Seven)

Trivia: In Thailand, stepping on currency is considered offensive because it features whose image? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $11.55 | Below average |

52‑week range | $1.83 - $11.12 | Below average |

Short interest | 44.96% | Above average |

Next catalyst | New geographic approvals or label expansions |

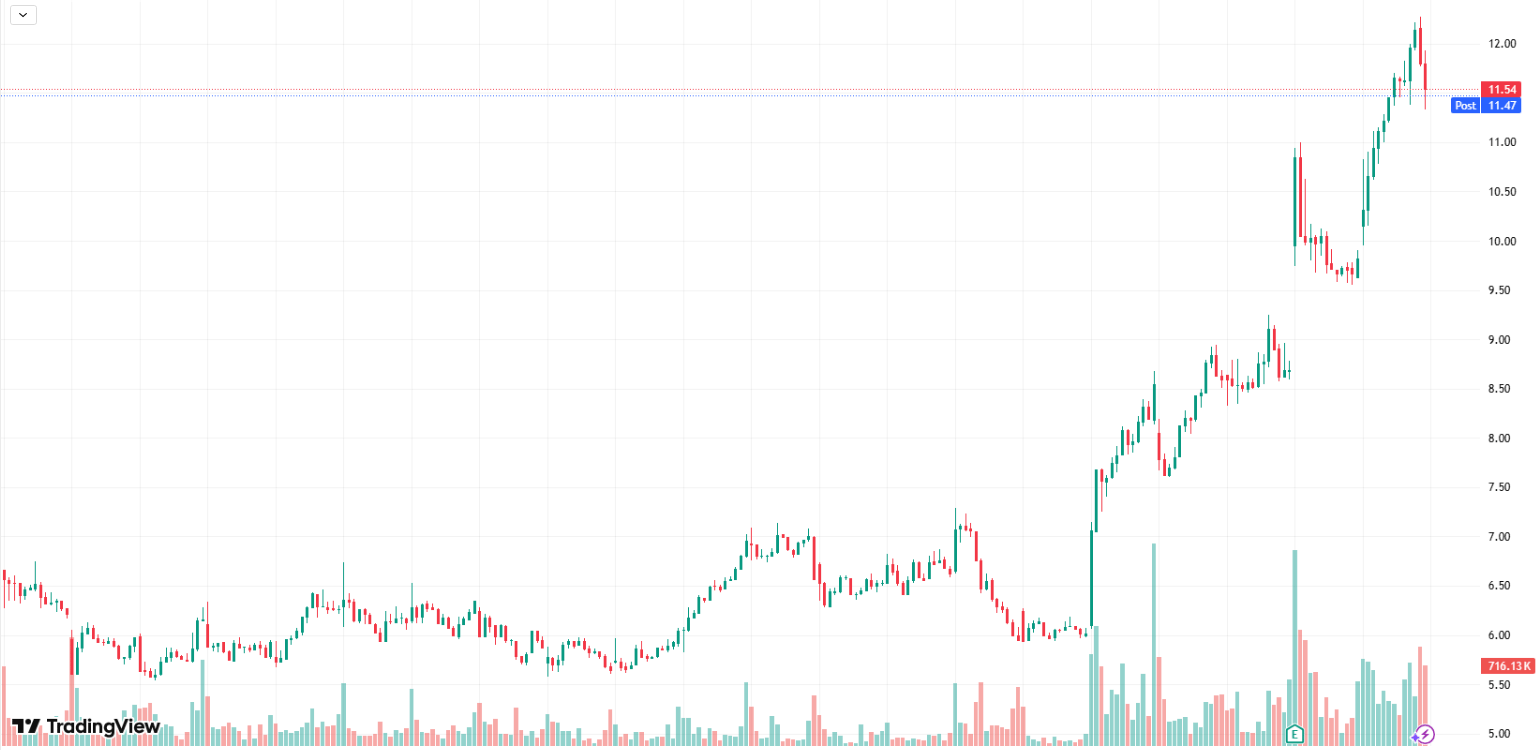

Chart

1-month trading summary: Over the past month, AIBRX has shifted gears from grind to surge, ripping more than 50.00% higher and accelerating sharply in the second half of the move as buyers piled in on real volume.

What started as a steady climb turned into a breakout, clearing prior consolidation and pressing into fresh highs with momentum that feels institutional, not retail.

This is not a sleepy biotech drift. It is a repricing move, fueled by revenue growth and reinforced by technical strength.

Bull Case

The commercial inflection that changes the game: For years, ImmunityBio lived in the penalty box. Delays, dilution, regulatory setbacks, and a constant need for capital turned it into a trader’s vehicle rather than an investor’s conviction play.

The market learned to discount the story before it even heard it. That identity is now under pressure.

700% year-over-year revenue growth is not incremental progress. It is proof of product-market fit. ANKTIVA is no longer a pipeline promise.

It is generating real dollars, scaling unit volume, and expanding geographically. That shifts the conversation from clinical speculation to commercial execution.

Near-term execution meets extreme positioning: The next earnings report is the pressure test. If ImmunityBio posts another quarter of meaningful sequential revenue growth and reinforces ANKTIVA demand trends, the commercial story hardens from narrative to evidence.

Consistent execution over the next two quarters would make it increasingly difficult to dismiss this as a temporary launch spike.

Now add the structural tension. With 44.96% of the float sold short, this is one of the more aggressively bet-against names in small-cap biotech. If fundamentals continue improving, that positioning becomes unstable.

Strong results do not just validate the bull case; they also confirm it. They force repricing as shorts reduce exposure to strength.

Layer in potential label expansion updates or additional geographic approvals, and the company moves from proving survival to proving scale. That is when multiples expand.

Wide dispersion reflects a market still making up its mind: Analyst price targets range from $7.00 on the low end to $23.00 on the high end, which tells you everything about where ImmunityBio sits in the cycle. This is not consensus comfort. It is a debate.

The low target reflects lingering skepticism around durability, dilution risk, and execution discipline.

The high target reflects the belief that revenue acceleration is real and that the company is transitioning into a legitimate commercial oncology growth story.

Momentum with pressure underneath: IBRX is in a clean short-term uptrend, breaking out on strong volume and holding its gains rather than fading them.

Pullbacks are being absorbed quickly, and former resistance is turning into support.

With nearly 45.00% of the float sold short, every push higher tightens the pressure.

Strong momentum, combined with crowded positioning, can feed on itself. As long as the trend holds, the tape stays constructive.

Bear Case

Execution stumbles and the old narrative snaps back: The biggest risk is that growth stalls.

If ImmunityBio posts a soft quarter, shows slowing ANKTIVA uptake, or signals continued heavy cash burn without a clear path to operating leverage, the market will not be patient.

This stock has a long memory. Investors remember dilution. They remember delays. They remember volatility.

Positioning cuts both ways. If revenue momentum wobbles, shorts are not trapped. They are validated. And in small-cap biotech, when confidence cracks, air pockets form quickly.

Competing against giants with deeper pockets: ImmunityBio is not operating in a quiet corner of oncology.

In bladder cancer and broader immuno-oncology, it competes directly or indirectly with heavyweights like Merck & Co., Inc. and its PD-1 powerhouse Keytruda, as well as diversified players such as Bristol-Myers Squibb Company and Roche Holding AG.

These companies have global sales forces, entrenched physician relationships, massive trial budgets, and the ability to bundle therapies across indications.

They can move fast, defend turf aggressively, and absorb pricing pressure far more easily than a small-cap.

The bear case says competing with giants is rarely linear and never easy. In oncology, scale matters. And scale is exactly what the incumbents already have.

Biotech never trades in a vacuum: IBRX can execute perfectly and still get dragged around by forces it does not control.

Drug pricing reform is a recurring political football, and oncology reimbursement is always under scrutiny. When Washington starts talking about cost containment, smaller commercial biotechs feel it first and hardest.

And oncology is not a quiet battlefield. Data drops from larger players, new combination regimens, or shifts in standard-of-care guidelines can reroute treatment flows overnight. The company may be improving. The backdrop can still turn hostile.

Crowded on both sides: IBRX is becoming crowded in two directions. When a stock gets popular on both sides, volatility expands. If momentum stalls even briefly, late longs can exit just as aggressively as shorts.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (February 24, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha