- Everyday Alpha

- Posts

- The Sneaker Chain Finding Its Rhythm Again as the Market Starts to Look Twice

The Sneaker Chain Finding Its Rhythm Again as the Market Starts to Look Twice

A footwear retailer is rebuilding momentum through stronger margins, sharper execution, and cultural relevance. The market is starting to notice, but the rerating story may still have room to run.

Noah Zelvis

March 23, 2026

A familiar retail name is starting to look different again, and the shift is showing up where it matters most.

As execution tightens and demand holds, the setup is beginning to tilt back in the buyer's favor.

Limited Window (Sponsored)

Bloomberg is calling Elon Musk's upcoming SpaceX IPO "the biggest listing of ALL TIME."

But here's the thing - most investors will be locked out until AFTER it goes public.

Not you.

I've found a 'backdoor' that lets everyday Americans grab a pre-IPO stake in SpaceX right now.

Click Here for the FREE "SpaceX" Ticker

Genesco, Inc.

March 23 – Pre‑market

Ticker: GCO | Sector: Apparel Retail/Consumer Cyclical | Market Cap: $268.09M

30‑Second Take

There’s a very specific kind of setup the market loves, and Genesco is starting to lean into it.

You’ve got a retailer that already proved it can execute through a messy consumer backdrop, now pairing that with improving footwear demand, cleaner inventories, and a business mix that’s quietly shifting toward higher-margin channels.

Journeys is stabilizing, Schuh is holding its ground internationally, and the company is showing early signs of margin repair just as sentiment around discretionary retail begins to thaw.

This is the kind of “was left for dead, now getting its act together” story that can rerate faster than people expect.

Trade Setup

Time frame: Short term

Edge type: Turnaround momentum

Genesco is shaping up as a sentiment shift story.

If improving retail trends and stronger footwear demand continue feeding into earnings expectations, the stock has room to rerate as investors start treating it less like a struggling mall retailer and more like a recovering brand platform.

Exclusive Opportunity (Sponsored)

While President Trump's official salary is $400,000 per year... his tax returns reveal he's been collecting up to $250,000 PER MONTH from one hidden source.

Until recently, most Americans couldn't touch the type of investment that makes up this investment.

But thanks to Executive Order 14330, that just changed. If you love investing in disruptive new companies...

Discover how to invest in the fund Trump uses to collect this income

Poll: Which financial decision would you redo if you could? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $24.84 | Below average |

52‑week range | $16.19 - $38.95 | Below average |

Short interest | 9.54% | Average |

Next catalyst | Earnings update |

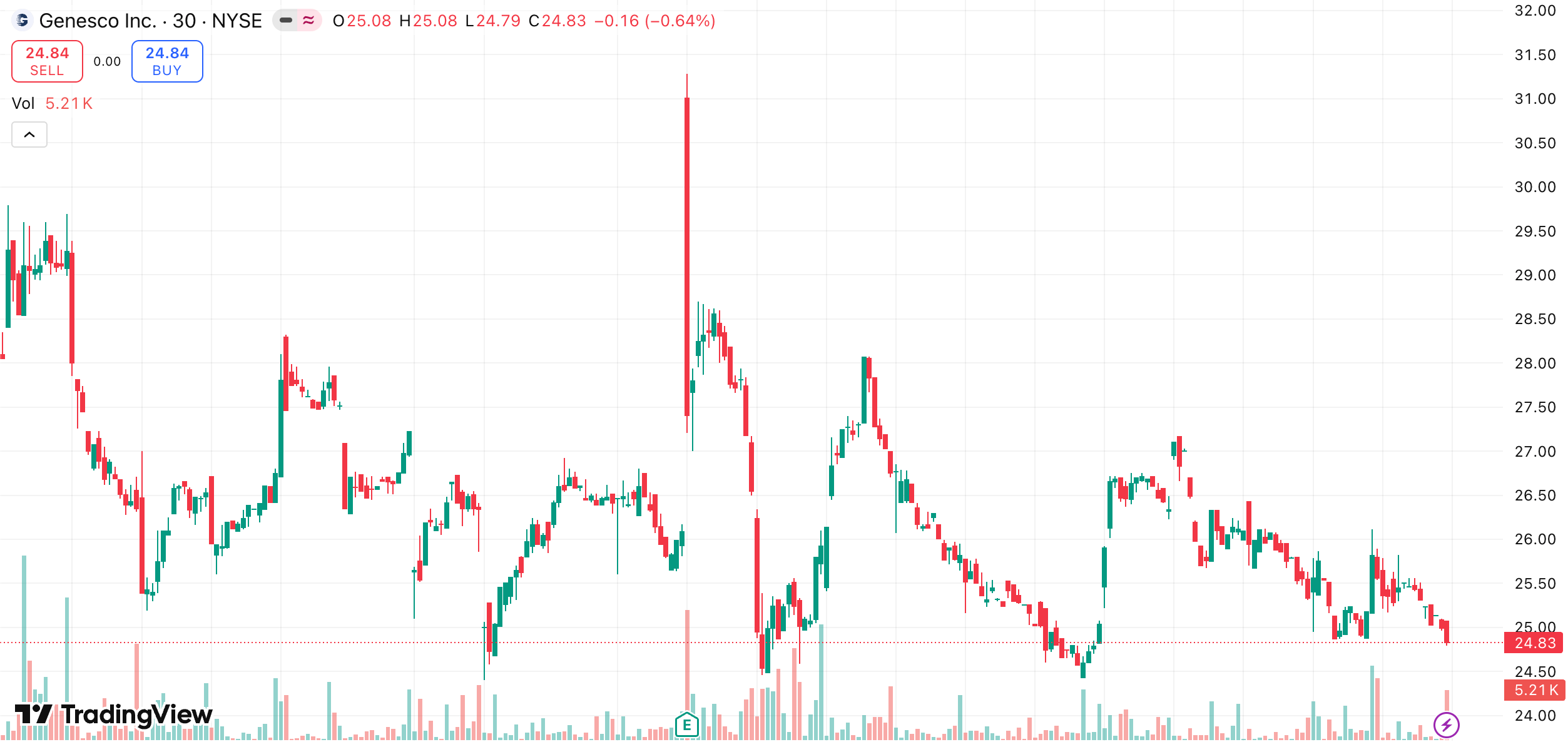

Chart

1-month trading summary: Genesco has taken a sharper step back over the past month, falling around 14.19% and sliding from the high-$20s toward the $25 level.

The chart shows a clear loss of short-term momentum, with each bounce struggling to hold and sellers gradually pressing the stock lower.

Step back, though, and the broader trend still holds together. Shares remain up 13.8% over the past year, suggesting this is more of a reset than a reversal.

For investors, that kind of pullback often opens the door to a more attractive entry before the next leg higher.

Bull Case

This is not just a retailer; it is a youth culture engine: Genesco's edge comes down to one thing. It sits right at the intersection of footwear, fashion cycles, and youth identity.

Through banners like Journeys, the company is not simply selling shoes; it is plugged into the trends that actually drive demand.

When sneaker culture heats up, Genesco feels it early and monetizes it quickly.

What makes the story compelling right now is the shift beneath the surface. Margins are stabilising, inventory is being managed more tightly, and digital channels are doing more of the heavy lifting.

That combination matters. It turns Genesco from a low-confidence mall retailer into a business that can flex with demand and protect profitability.

There is also a valuation gap that has not fully closed. The market is still pricing in a version of Genesco that struggles with foot traffic and discounting.

At the same time, the reality is a business that is becoming more disciplined, more brand-led, and more responsive to consumer trends.

If that perception starts to change, the rating potential for a rerating here is very real.

Momentum meets the next proving ground: The path higher for Genesco is going to be driven by proof.

Proof that margins are holding, that demand for lifestyle footwear remains resilient, and that the business can convert that demand into cleaner earnings.

Near term, earnings updates will be key.

Any signs of stronger-than-expected sales at Journeys, improved inventory discipline, or margin expansion could quickly shift sentiment.

Beyond that, continued growth in digital channels and a more focused product mix give the company multiple ways to surprise to the upside.

If Genesco starts stringing together a few clean quarters, this stops being a recovery story and becomes a rerating in motion.

Price target: Analysts see clear upside, with a high target of $43.00. The low is $29.00.

Pressure building beneath the surface: After a sharp pullback, Genesco is starting to look stretched to the downside, with the stock hovering near recent support around the mid-$20s.

If buyers step back in, this setup can flip quickly, with room for a rebound toward the high-$20s where the last breakdown began.

Bear Case

When fashion cools, the numbers follow: The biggest risk here is simple. Genesco is closely tied to trends, and trends can turn quickly.

If demand for lifestyle footwear softens or key brands lose momentum with younger consumers, sales can slip more quickly than the market expects.

There is also the margin side of the story. If inventory builds or discounting creeps back in, the progress on profitability could reverse just as quickly as it appeared.

In that scenario, the market stops viewing this as a recovery and starts pricing it like a pressured retailer again, which would cap any near-term upside.

Fighting for the same sneaker dollar: Genesco is not operating in a vacuum.

It is competing with names like Foot Locker, JD Sports, and even broader apparel players like Urban Outfitters, all chasing the same trend-driven, youth-focused consumer.

The difference is in positioning. JD Sports leans premium and global scale, Foot Locker has deep brand relationships, and fast-fashion retailers move quickly on trends.

Genesco sits somewhere in the middle, which can be an advantage when it is executing well, but leaves less room for error if competitors start capturing the cultural momentum instead.

When the consumer hesitates, so does the checkout: This is still a consumer discretionary story at heart. If spending tightens, footwear is one of the easiest places for shoppers to pause or trade down.

Add ongoing inflationary pressure and the stop-and-go nature of mall traffic, and the backdrop can shift quickly.

There is also the broader retail dynamic. Promotions can return quickly when demand softens, which tends to squeeze margins across the sector.

If the environment becomes more competitive, Genesco will not be able to operate on its own terms.

Not crowded, but not ignored either: This is not a trade everyone is piled into, which helps. But that also means conviction is still fragile.

If sentiment wobbles or the next update disappoints, there are not many sticky holders to steady the move, and the stock can drift just as quickly as it rallies.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (March 22, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha