- Everyday Alpha

- Posts

- The Market Still Sees an Oil Stock, but the Business Underneath Has Changed

The Market Still Sees an Oil Stock, but the Business Underneath Has Changed

This energy name is still being priced like a volatile commodity trade, but the underlying business is becoming stronger, more diversified, and far more resilient than the market seems to realize.

Energy stocks rarely stay ignored forever once cash flow starts piling up. That is what makes this setup interesting right now.

What looks like another cyclical oil producer on the surface is increasingly turning into a more balanced energy business with stronger downside protection and meaningful upside if crude sentiment improves again.

Market Shift (Sponsored)

Wall Street legend Marc Chaikin's award-winning system turned bearish on software stocks two months before they crashed this year.

Now, he's warning that one AI lab's breakthrough could CRASH the Nasdaq while igniting a $500 trillion wealth transfer.

He's found a little-known $40 "pre-IPO backdoor" into the private startup behind this economic sea change.

Click here for its name and ticker symbol before June 16.

This ad is sent on behalf of Chaikin Analytics, 201 King Of Prussia Rd., Suite 650, Radnor, PA 19087. If you would like to optout from receiving offers from Chaikin Analytics please click here.

Cenovus Energy Inc.

May 11 – Pre‑market

Ticker: CVE | Sector: Oil & Gas Integrated / Energy | Market Cap: $53.1B

30‑Second Take

Oil stocks have spent the past year trapped between two competing narratives. On one side, investors are worried about slowing global growth and softer crude prices. On the other hand, several producers are quietly becoming far stronger businesses underneath the surface. CVE sits right in the middle of that disconnect.

What makes this setup interesting now is that Cenovus is no longer just a pure oil sands story. The company has spent the last few years building a more diversified energy platform through refining, downstream integration, and operational scale.

That’s important here because integrated producers tend to hold up better when crude prices wobble, while still benefiting heavily when energy markets tighten again.

Trade Setup

Time frame: Medium term

Edge type: Energy cycle rerating + cash flow durability

The key focus here is a shift in perception. Cenovus has already done much of the hard operational work, but the stock is still trading as if oil producers are permanently stuck in a low-multiple penalty box.

That creates an interesting asymmetry. If crude prices remain stable, Cenovus still generates substantial free cash flow. If energy markets tighten again, operating leverage can become very powerful very quickly. Investors are essentially getting paid to wait for sentiment to catch up to the underlying business quality.

Global Tensions (Sponsored)

There’s a strategy behind the Iran war.

I know because I heard it directly in a closed-door meeting with a source whose connections run deep into global power networks.

He walked me through the real purpose and the massive deal tied to it.

How much did Airbnb's founders spend testing their original idea in 2007, renting air mattresses in their San Francisco apartment? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $28.40 | Below average |

52‑week range | $12.88 - 30.85 | Below average |

Short interest | 2.21% | Below average |

Next catalyst | Refining margin strength |

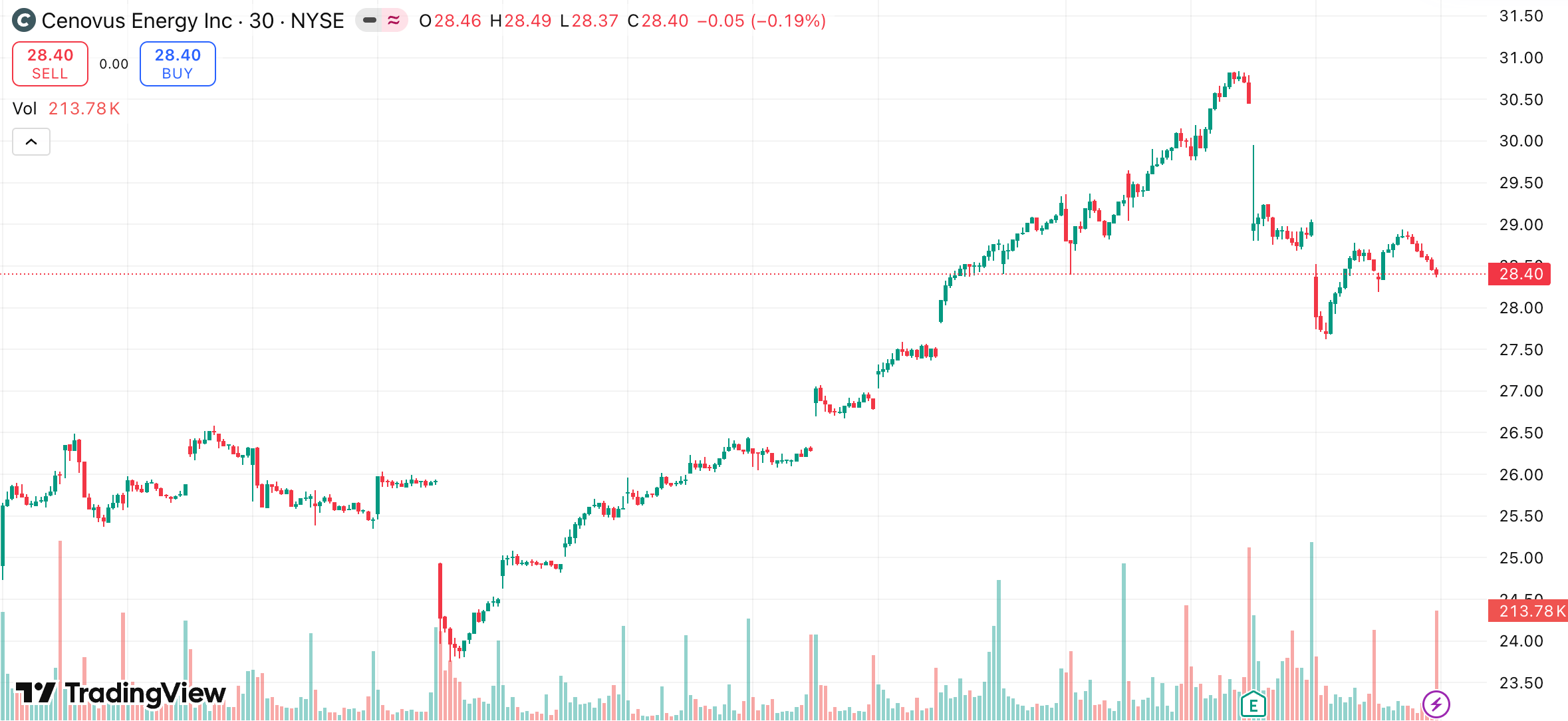

Chart

1-month trading summary: Cenovus has started to wake up again after spending much of the past year grinding sideways with the broader energy sector.

The stock climbed more than 4% over the past month and briefly pushed above $30 before pulling back amid cooling crude sentiment this week.

What stands out is the character of the move. Buyers stepped in aggressively through late April as energy stocks caught a bid, volume improved, and the stocks broke out of their recent ranges.

Even with the latest pullback, shares are still holding well above the April lows, which suggests investors are beginning to treat dips as opportunities rather than exits.

Bull Case

More than just an oil sands producer: The bull case for CVE comes down to one simple idea: the market still undervalues the extent of the business's evolution.

This is no longer a narrow bet on rising crude prices. Cenovus now has a far more balanced model through its refining assets, downstream operations, and production scale, which gives the company multiple ways to generate cash flow across different energy environments.

That diversification matters because it reduces the volatility investors traditionally associate with Canadian oil sands names.

There is also a valuation gap that still looks difficult to ignore. The stock trades at levels that suggest the market expects a weaker cycle ahead. Yet the company continues to produce meaningful free cash flow, return capital to shareholders, and improve operational efficiency.

If oil stabilizes rather than collapses, the current multiple starts to look too cheap for the quality of the asset base.

When cash flow starts demanding attention, the biggest catalyst is simple: sustained execution in a tougher oil environment. If Cenovus continues to deliver strong free cash flow, buybacks, and operational consistency while crude prices remain choppy, the market will have a harder time treating the stock as a purely cyclical trade.

There’s also the refining angle to consider. Integrated energy businesses tend to become far more attractive when refining margins strengthen alongside stable production volumes, and Cenovus has built meaningful exposure there over the last few years. That creates the potential for earnings resilience even if headline oil prices stop surging.

Price targets: Analyst targets range from a low of $25.17 to a high of $32.00, with the spread reflecting how sensitive sentiment remains to the broader direction of oil prices.

Energy money rotating back in: The stock is still holding above its April breakout zone despite the recent pullback, which suggests underlying buying demand remains intact. If crude firms up again, Cenovus looks well-positioned to attract momentum traders hunting for large-cap energy names that have not fully rerated yet.

Bear Case

Still tied to the oil tape: No matter how much Cenovus improves operationally, this is still an energy stock living at the mercy of crude sentiment.

If oil prices roll over hard or recession fears accelerate, the knee-jerk reaction will likely be to sell first and revisit the fundamentals later. That is the frustrating reality of owning commodity-linked businesses, even the stronger ones.

Trying to stand out in a sea of oil giants: Cenovus is competing against multiple heavyweight names for investor attention, including Canadian Natural Resources, SU, Imperial Oil, and XOM.

The good news is that Cenovus no longer feels like the awkward smaller sibling in that group. The company has become more diversified, more operationally disciplined, and far more capable of generating dependable cash flow across different energy environments.

Oil prices still drive the mood: The biggest sector risk remains global growth. If economic data weakens or recession fears return, crude prices can fall quickly and drag energy stocks lower, regardless of company-specific execution.

OPEC policy shifts and softer Chinese demand also remain major swing factors for the entire sector.

Energy has become fashionable again: Part of the easy money in energy has already been made, which means Cenovus now needs execution and cash flow strength to keep attracting buyers rather than relying purely on the sector trade.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (May 10, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha