- Everyday Alpha

- Posts

- The Beaten-Down Metals Giant That Could Snap Back Fast

The Beaten-Down Metals Giant That Could Snap Back Fast

After a steep selloff and fading sentiment, this volatile precious metals producer looks washed out. If metals stabilize and cash flow holds, the rebound potential could be dramatic.

Noah Zelvis

March 09, 2026

Cyclical stocks do not ring a bell at the bottom. They exhaust sellers, compress expectations, and then quietly start to turn.

This metals name may be closer to that turn than it first seems. Could it be the sheen your portfolio needs?

Sibanye Stillwater Limited

March 09 – Pre‑market

Ticker: SBSW | Sector: Other Precious Metals & Mining / Basic Materials | Market Cap: ~$163.18B

30‑Second Take

Gold is firming. Rate cut chatter is back. Real yields are losing their grip. Capital is quietly rotating back toward hard assets.

But Sibanye is still priced like the commodity cycle is permanently broken.

After months of pressure from weak platinum group metal prices and South African risk headlines, the stock trades with deep skepticism baked in. Expectations are low. Sentiment is tired. Positioning is light.

That is exactly the setup we look for. If gold stays bid and PGMs stop getting worse, the earnings torque here is meaningful.

This is a high-beta precious metals name trading at depressed cycle assumptions just as the macro backdrop begins to shift. That mismatch is why this is our pick today.

Early Access (Sponsored)

For decades, Wall Street insiders have secured the biggest IPO gains before the public ever gets a shot.

Now, one economist says everyday investors may have a rare window to position ahead of a potential $1.5 trillion SpaceX offering.

See how this strategy works by clicking here - and what you should know before the next major IPO announcement.

Trade Setup

Time frame: Short to medium term

Edge type: Cyclical inflection with high operating leverage

This is a rebound trade in a stock that has already been dragged through the cycle.

The market has priced in weak PGM demand, execution risk in South Africa, and persistent margin pressure. What it has not priced in is stabilization. Sibanye does not need a metals boom to work. It needs gold to hold firm and platinum group metals to stop deteriorating.

Because of its cost structure and operating leverage, small pricing improvements can drive outsized changes in earnings expectations. When sentiment is this compressed, the shift from negative to "less bad" can be enough to trigger a sharp move.

This is about positioning ahead of that inflection, not chasing it after the rerating begins.

Trivia: What company bought Minecraft for $2.5 billion in 2014? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $14.10 | Below average |

52‑week range | $3.18 - $21.29 | Below average |

Short interest | 1.87% | Below average |

Next catalyst | Cash flow inflection |

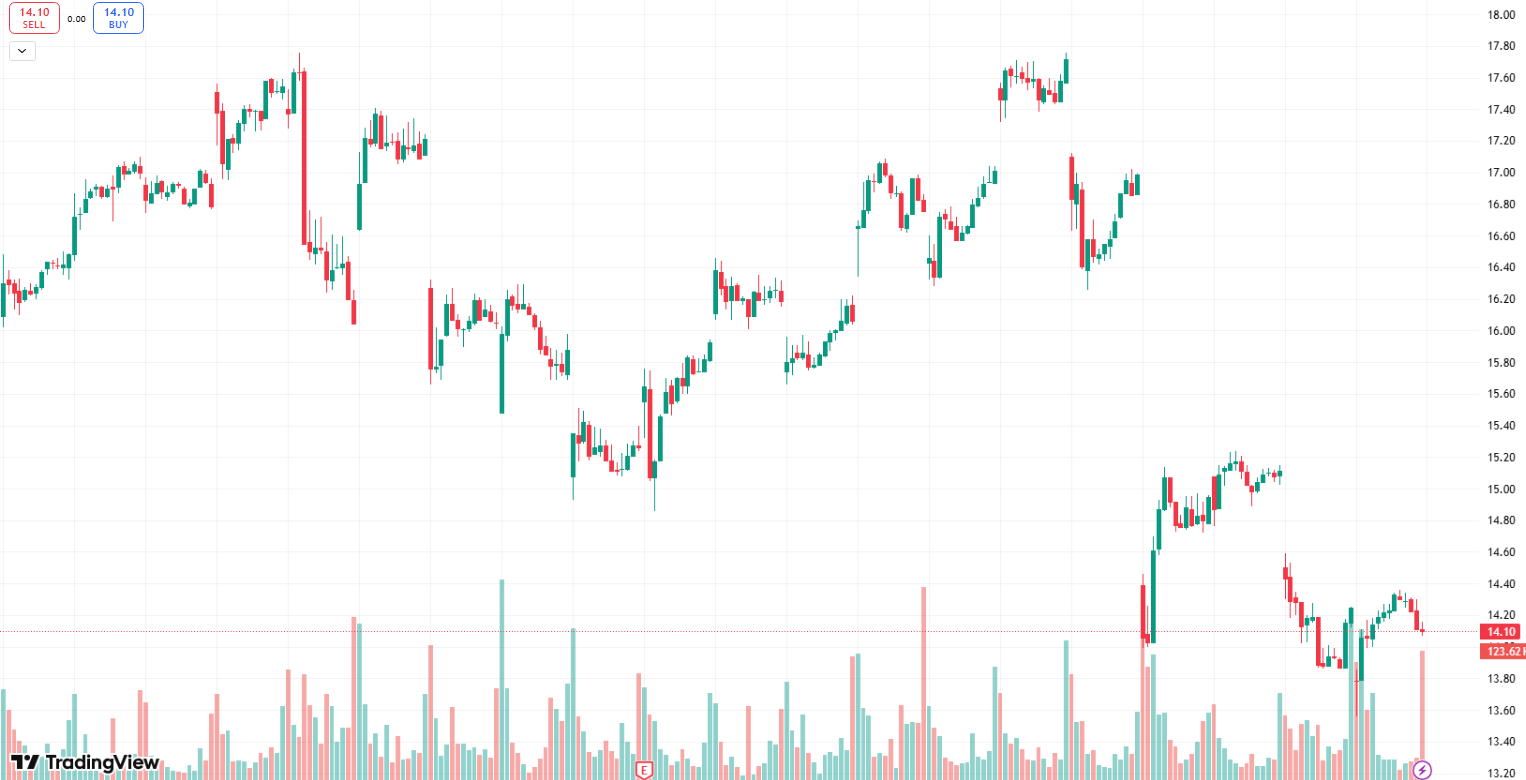

Chart

1-month trading summary: The past month has been bruising. The stock slid from the mid-$17.00s to the low-$14.00 range as metals weakness and sector pessimism pushed sellers firmly in control.

But that kind of swift reset can change the setup quickly. When a high-beta miner gets hit this hard in a short window, expectations fall fast and even modest stabilization in metals can spark a sharp rebound.

Bull Case

A misunderstood metals machine hiding torque in plain sight: Sibanye is not just a gold miner. It is a diversified precious and strategic metals company with enormous operating leverage.

Cycles in platinum and palladium do not die quietly. They compress, they overshoot, and then they snap back. When they do, the companies that survived the downturn with scale tend to move first and hardest.

Sibanye has scale. It has diversified exposure. It has taken pain, cut costs, and endured the worst part of the cycle. That matters. Survivors in commodity downturns often come out leaner and more disciplined.

The pressure points that could spark a surge: SBSW is sitting on compressed expectations.

If management proves that the worst of the restructuring is behind them and free cash flow starts surprising to the upside, the entire narrative changes.

This stock has been treated like a balance sheet problem. The moment it starts behaving like a cash generator again, multiples can expand quickly.

There is also operating leverage waiting to be rerated. A modest lift in realized pricing across gold or PGMs does not trickle through here. It amplifies.

Low-to-high price targets: Price targets range from $16.30 to $24.15.

Waiting for the turn: There’s no denying the last few sessions have been unforgiving but that kind of rapid reset can create opportunity.

When a high-beta miner becomes this stretched to the downside, even small improvements in metals pricing or sentiment can trigger fast snapback rallies.

Energy Race (Sponsored)

Something big is happening in energy — right now.

An MIT genius has cracked a way to tap an energy source that never runs out.

The U.S. Department of Energy says it could supply power for billions of years.

Big Tech isn’t waiting — they’re already positioning themselves.

Here’s what’s driving the rush.

Bear Case

When leverage cuts the other way: The same operating leverage that makes this exciting can turn painful quickly.

If platinum group metals stay weak or roll over again, cash flow pressure returns fast. Sibanye does not have the luxury of shrugging off pricing softness. Margins compress quickly in this business.

There is also jurisdiction risk. South African labor dynamics, power reliability, and regulatory noise can reappear without warning.

Bigger rivals, different risk profiles: If you want scale and geopolitical insulation, you look at names like Newmont Corporation or Barrick Gold.

They offer cleaner gold exposure, stronger balance sheets, and operations spread across multiple jurisdictions. They are the institutional comfort picks.

If you want a more focused PGM operator, Impala Platinum and Anglo American Platinum provide purer exposure to platinum and palladium cycles.

Sibanye sits in the messy middle.

It is not the safest gold major. It is not the cleanest PGM pure play. It is more complex, more volatile, and more misunderstood. That complexity is precisely why it can rerate harder if sentiment turns.

The macro crosscurrents:

Sibanye lives and dies by metals pricing, and right now that means two very different macro forces pulling in opposite directions.

If real yields push higher again or the dollar strengthens, gold can lose momentum quickly. That would cap upside just as the stock is trying to stabilize.

At the same time, platinum and palladium demand remain tied to global auto production and industrial activity. A slowdown in China or softer EV and hybrid demand would keep pressure on PGM pricing longer than bulls expect.

There is also energy and cost inflation risk specific to South Africa. Power reliability, wage negotiations, and currency swings can squeeze margins even if headline metals prices look stable in US dollars.

Crowded trade risk: If gold and PGMs spike quickly, fast money could crowd into this high-beta name and crowd out just as quickly, creating sharp whipsaws.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (March 08, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha