- Everyday Alpha

- Posts

- From Scrap Heap to Second Look: The Clean-Up Story Starting to Stick

From Scrap Heap to Second Look: The Clean-Up Story Starting to Stick

A messy industrial past is being stripped away, replaced by higher-quality environmental revenue and improving margins. If the numbers start to confirm it, this could rerate quickly.

Noah Zelvis

April 02, 2026

This is what it looks like when a business starts shedding its old identity, and the market has not fully caught up yet.

If the clean-up shows up clearly in the numbers, this could move faster than most expect.

Advisor Help (Sponsored)

Capital gains taxes may quietly reduce more of your investment returns than you realize.

But the tax code includes several strategies that may help reduce that bill.

Three often-overlooked areas include investment-related expenses, cost basis adjustments, and real estate selling costs.

When structured correctly, these deductions may help minimize taxable gains.

Because the rules can be complex, many investors work with fiduciary financial advisors to plan tax-efficient strategies.

Use SmartAsset’s free tool to find vetted financial advisors serving your area.

Enviri Corporation

April 02 – Pre‑market

Ticker: NVRI | Sector: Waste Management / Industrials | Market Cap: $1.60B

30‑Second Take

This is what a repositioning story looks like just before the market fully clocks it.

What used to be a tangled industrial name is being stripped back and refocused into environmental services and infrastructure-linked revenue that investors actually want exposure to.

The interesting bit is the timing. Margins are starting to firm, the mix is improving, and the narrative is catching up just as capital rotates back into real assets and sustainability plays.

When perception shifts on names like this, it rarely moves in a straight line or at a slow pace.

Trade Setup

Time frame: Near term (4 to 12 weeks)

Edge type: Rerating + mix shift

Hidden Income (Sponsored)

His official salary? $400,000 a year.

But his tax returns reveal something unexpected:

Up to $250,000 per month from a single source.

It’s not real estate.

It’s not stocks.

So what is it — and why are more investors paying attention now?

Discover how you could get started for under $20

Trivia: Which U.S. president signed the legislation that created the 401(k)? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $19.75 | Below average |

52‑week range | $4.72 - $19.97 | Below average |

Short interest | 11.67% | Above average |

Next catalyst | Environmental mix proof |

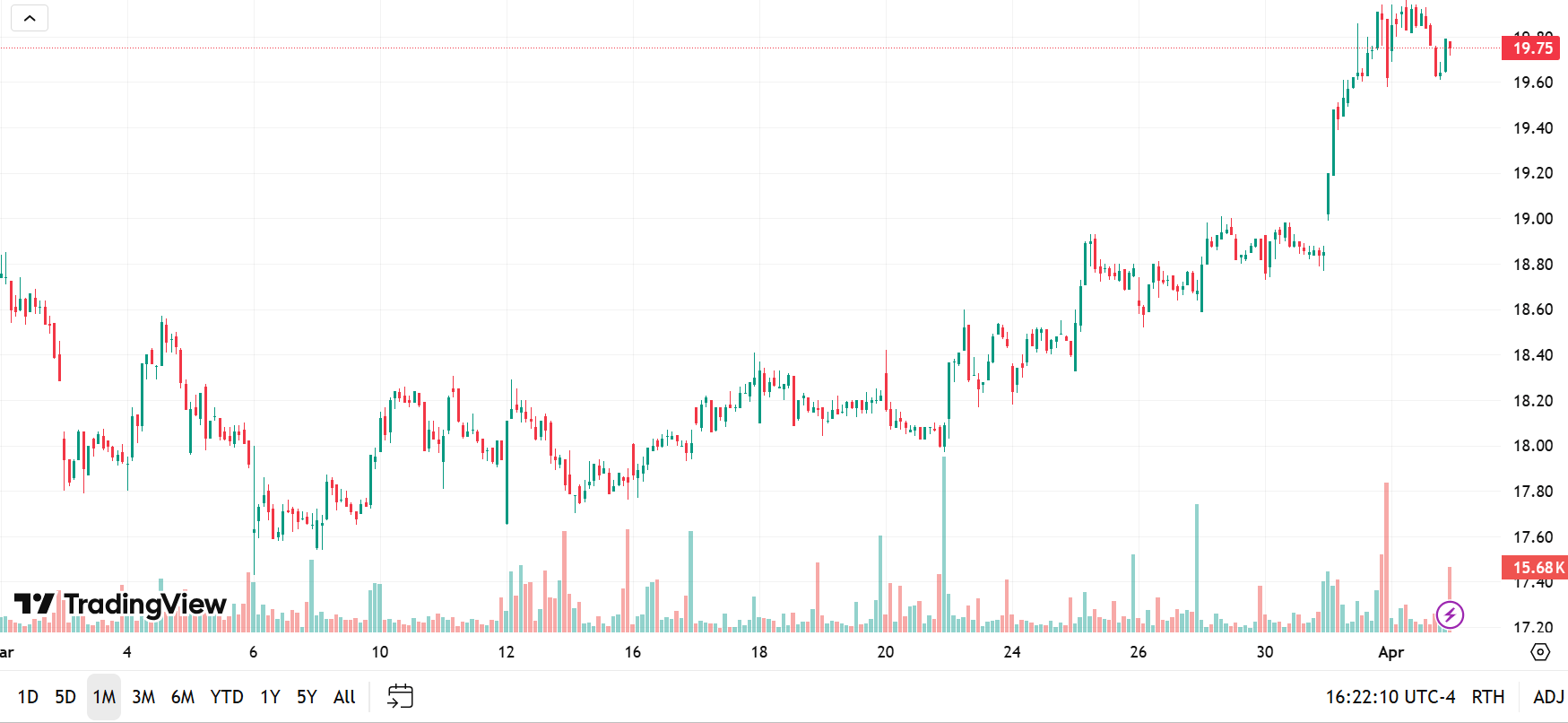

Chart

1-month trading summary: The past month has that steady climb feel, but look closer, and it is tightening with intent.

Shares have pushed up toward the $20.00 level, now brushing against the top of the 52-week range, with higher lows stepping in along the way.

Momentum has picked up into the back end of the move, and that late push higher suggests this is not just drift; it is buyers getting more confident.

The key now is whether it can hold this breakout zone rather than fade back into the range.

Bull Case

A cleaner story, the market is starting to pay for: This is no longer the business many investors still think it is.

The legacy complexity is being stripped away, leaving a far more focused environmental services platform focused on waste, recycling, and infrastructure support.

That matters because these are areas where demand is steadier, contracts are stickier, and pricing power is more consistent.

The real shift is in the mix. Higher-quality revenue streams are starting to do more of the heavy lifting, and that is where margins begin to open up.

As that becomes clearer in the numbers, the valuation framework changes. This stops being treated like a lumpy industrial and starts being compared to more stable, cash-generative service names.

What makes this interesting right now is that the market has not fully caught up. You are seeing early signs of execution, but not enough yet to force a broad rerating.

If that continues, the gap between how the business is performing and how it is priced tends not to last long.

Environmental services take the lead: It starts with cleaner numbers.

A quarter where margins move decisively higher, or cash flow comes through stronger than expected, is enough to force a rethink, especially if it is driven by the environmental services side doing more of the work.

Then it becomes about proof of mix. More visibility on contract wins, pricing strength, or growth in higher-margin segments gives investors something concrete to anchor to.

That is when the story shifts from “in transition” to “already happening.”

There is also a strategic angle sitting under the surface.

Any further simplification, asset reshaping, or balance sheet improvement sharpens the narrative and removes excuses for the market to stay on the sidelines.

Once that combination lands together, numbers, mix, and clarity, this is the kind of name that can catch attention quickly.

What does Wall Street think? Analysts are divided with $19.00 on the low end if the story stalls, but $25.00 if the mix shift and margin story start landing cleanly in the numbers.

Holding the breakout, building pressure: Price is pushing into fresh highs with a clear series of higher lows underneath, which is exactly what you want to see at this stage.

That kind of structure tends to attract momentum buyers rather than shake them out.

Bear Case

Taking out the trash, or just moving it around? The risk here is that NVRI still looks better on paper than it does in the numbers.

If margin improvement stalls or the higher-quality segments fail to carry enough weight, the market quickly falls back to treating this like the same old industrial story it has always struggled to believe in.

There is also execution risk baked in.

This repositioning only works if management delivers consistently, and any wobble in contracts, pricing, or cash flow can dent confidence fast.

When a rating is built on changing perception, it does not take much to unwind it.

Not the only one cleaning up: This is a competitive space with some very well-established players who already have scale, pricing power, and long-standing contracts locked in.

The likes of Waste Management and Republic Services are not easy to disrupt, and they tend to win on consistency and investor trust.

That leaves Enviri needing to prove it can carve out its own lane rather than follow the leaders.

If it cannot differentiate on margins, service offering, or execution, it risks being seen as a smaller, less proven version of names the market already understands and prefers.

When the clean-up trade hits a dirty patch: This is still tied to industrial activity more than the market might want to admit.

If steel production, manufacturing, or broader infrastructure demand softens, volumes can slip, and pricing gets harder to push through, especially in the more cyclical parts of the business.

There is also a cost angle. Energy, transport, and labor all feed directly into margins here, and if those stay elevated while demand wobbles, it squeezes from both sides.

For a story that relies on improving margins, that kind of backdrop can slow the whole narrative down.

When everyone spots the clean-up story: NVRI is starting to get noticed, and once these repositioning trades catch a following, expectations can run ahead of delivery.

If too many people pile in at the same time, it does not take much of a wobble in the numbers to trigger a sharp shakeout.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (April 01, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha