- Everyday Alpha

- Posts

- From Problem Child to Comeback Story in the Making

From Problem Child to Comeback Story in the Making

A beaten-down industrial name is quietly rebuilding beneath the surface, and if the narrative shifts from risk to recovery, the upside could come faster than the market expects.

Noah Zelvis

March 20, 2026

Sometimes the best opportunities are the ones everyone has already written off. This is what it looks like when a complicated story starts getting simpler and more investable.

Don’t Miss (Sponsored)

Bloomberg is calling Elon Musk's upcoming SpaceX IPO "the biggest listing of ALL TIME."

But here's the thing - most investors will be locked out until AFTER it goes public.

Not you.

I've found a 'backdoor' that lets everyday Americans grab a pre-IPO stake in SpaceX right now.

Click Here for the FREE "SpaceX" Ticker

The Chemours Company

March 20 – Pre‑market

Ticker: CC | Sector: Specialty chemicals / Basic materials | Market Cap: $2.84B

30‑Second Take

Chemours feels like one of those names the market shoved into the “too difficult” pile and then stopped paying attention to. PFAS headlines did the damage, sentiment collapsed, and suddenly nobody wanted to touch it.

But under the surface, this isn’t a business falling apart. It’s one quietly resetting itself while expectations sit on the floor.

That’s where it gets interesting. Pricing is holding up better than feared in key segments, volumes are starting to find their footing, and management is tightening the screws on costs and cash.

When a stock moves from firefighting to rebuilding with nobody watching, the upside can catch people off guard.

Trade Setup

Time frame: Medium term

Edge type: Sentiment reset with earnings recovery rerating

This isn’t just a quick bounce idea. The real edge sits in the slow rebuild of credibility.

Now Available (Sponsored)

For decades, one type of investment was reserved for the ultra-wealthy.

Then Trump signed Executive Order 14330 - and opened it to everyone.

Now you can get into this boom for less than $20.

See what changed

Poll: You must pick one “boring” business to own — which do you choose? |

Snapshot Table

Metric | Value | Current Stance |

|---|---|---|

Price | $18.94 | Below average |

52‑week range | $9.13 - $21.85 | Below average |

Short interest | 9.11% | Above average |

Next catalyst | Earnings validation |

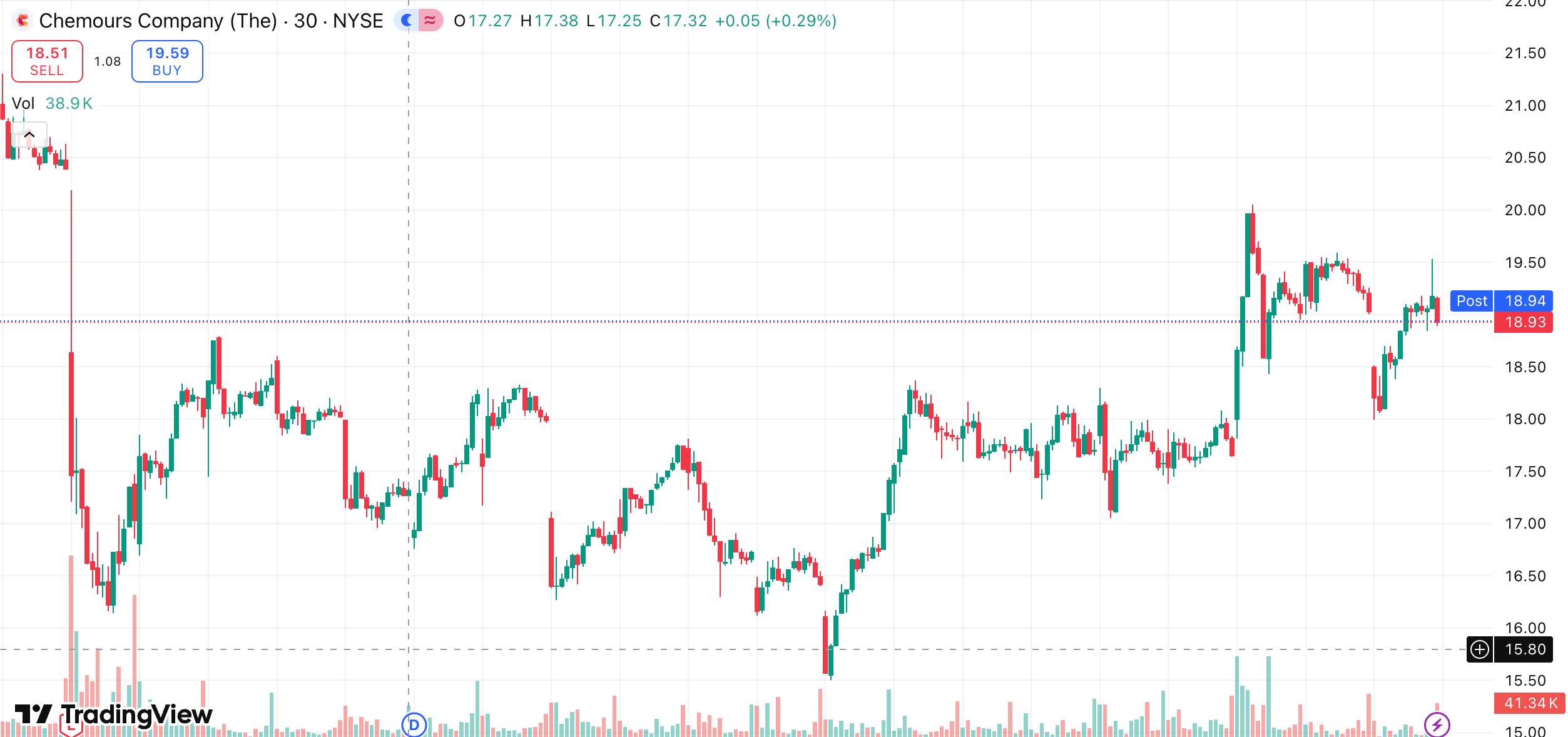

Chart

1-month trading summary: It has been a choppy month, but the tone is starting to shift. Chemours pulled back sharply early on, dropping into the mid $16.00s before finding its footing and building a steadier base.

From there, the move has been constructive. The stock has climbed back toward the $19.00 level with a series of firmer pushes higher, suggesting buyers are starting to step back in.

It is still down around 6.5% over the month, but the recent price action feels far more controlled, and importantly, more optimistic than where it started.

Bull Case

From regulatory overhang to industrial rebuild: Chemours sits right at the intersection of modern industry and everyday life. It produces performance chemicals used across cooling systems, coatings, plastics, electronics, and energy.

In simple terms, it’s a behind-the-scenes enabler of everything from air conditioning and packaging to semiconductors and EV infrastructure.

The opportunity here is less about what Chemours does and more about how the story is changing. For the past couple of years, the stock has been defined by what could go wrong, litigation, environmental liabilities, and cyclical pressure.

What makes this compelling now is the mismatch. You've got a company with strong, globally embedded product lines and real pricing power in hard-to-replicate niches, yet it's still valued like a problem case.

If Chemours can continue to stabilize earnings and show cleaner cash flow, the narrative shifts from “risk” to “recovery,” and that’s where reratings tend to accelerate.

This is not about perfection. It's about progress being recognized. And right now, the market looks like it's only just starting to notice.

Hitting the on button for growth: A steady run of “nothing went wrong” updates could be enough to move this stock skywards. Think steady volumes in Titanium Technologies, firmer pricing in refrigerants, and continued cost discipline flowing through to margins.

Any clarity or progress on PFAS liabilities removes a major overhang, while incremental balance sheet improvement adds confidence. Layer in even a modest demand uptick across coatings, cooling, and electronics, and suddenly this starts to look less like a recovery story and more like a rerating in motion.

Price targets: Analysts see a range from $17.00 on the downside to $23.00 on the upside, suggesting modest risk with a clear path to upside if sentiment continues to improve.

The tide is turning, and the tailwinds are gathering strength: Price action is beginning to stabilize after a messy stretch, with early signs of higher lows creeping in. That is usually where control starts to shift.

Bear Case

The overhang that refuses to go away: The biggest risk here is that the legal and environmental overhang does not fade as quickly as the market hopes.

PFAS-related liabilities remain a moving target, and any negative update or higher-than-expected settlement costs could reset sentiment quickly.

At the same time, this is still a cyclical chemicals business. If demand softens across coatings, construction, or industrial end markets, pricing power can slip, and margins can get squeezed.

In that scenario, the recovery narrative stalls, and the stock risks drift back into the "too difficult" bucket that investors just started to move away from.

Not short of heavy hitters: Chemours is not playing in an easy sandbox. It is up against some serious operators who know this space inside out. Think DuPont, the former parent that still looms large, Tronox Holdings in the TiO2 game, and Huntsman Corporation fighting for share across performance materials.

These are not passive competitors. They are disciplined, well-capitalised and constantly pushing on pricing, efficiency and innovation. That means Chemours does not get an easy recovery.

It has to earn it, quarter by quarter, while holding its ground against rivals that are more than capable of turning up the pressure if it slips.

When the cycle pushes back: Chemours is still tied to the rhythm of global industry, and that can turn quickly. If construction slows, coatings demand softens, or industrial production stalls, volumes feel it almost immediately.

Add in energy and input cost volatility, and margins can get squeezed just as the recovery is taking hold.

Then there is the regulatory backdrop. Environmental scrutiny is not easing, and any tightening of regulations on chemicals or emissions can raise compliance costs and limit flexibility.

Even if the company executes well, the wider backdrop can still make the path forward more uneven than the bull case would like.

Still early, but not under the radar for long: This is not a crowded trade yet, and that is part of the appeal. But that can change quickly. If the recovery narrative starts to stick and a few strong updates land, the same investors who ignored it will rush back in.

When that happens, the easy upside gets taken fast. You want to be early to the shift, not chasing it once everyone suddenly agrees.

Quick Checklist

✅ Thesis still valid after today’s close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (March 20, 2026)

Deep‑Dive Links

That’s all for today’s Everyday Alpha. We’ll have a new pick for you every morning before the market opens, so stay tuned!

Best Regards,

—Noah Zelvis

Everyday Alpha